The Bank of Ghana (BoG) has credited a surge in gold-related income and improved reserve management for a significantly stronger policy solvency position in 2025.

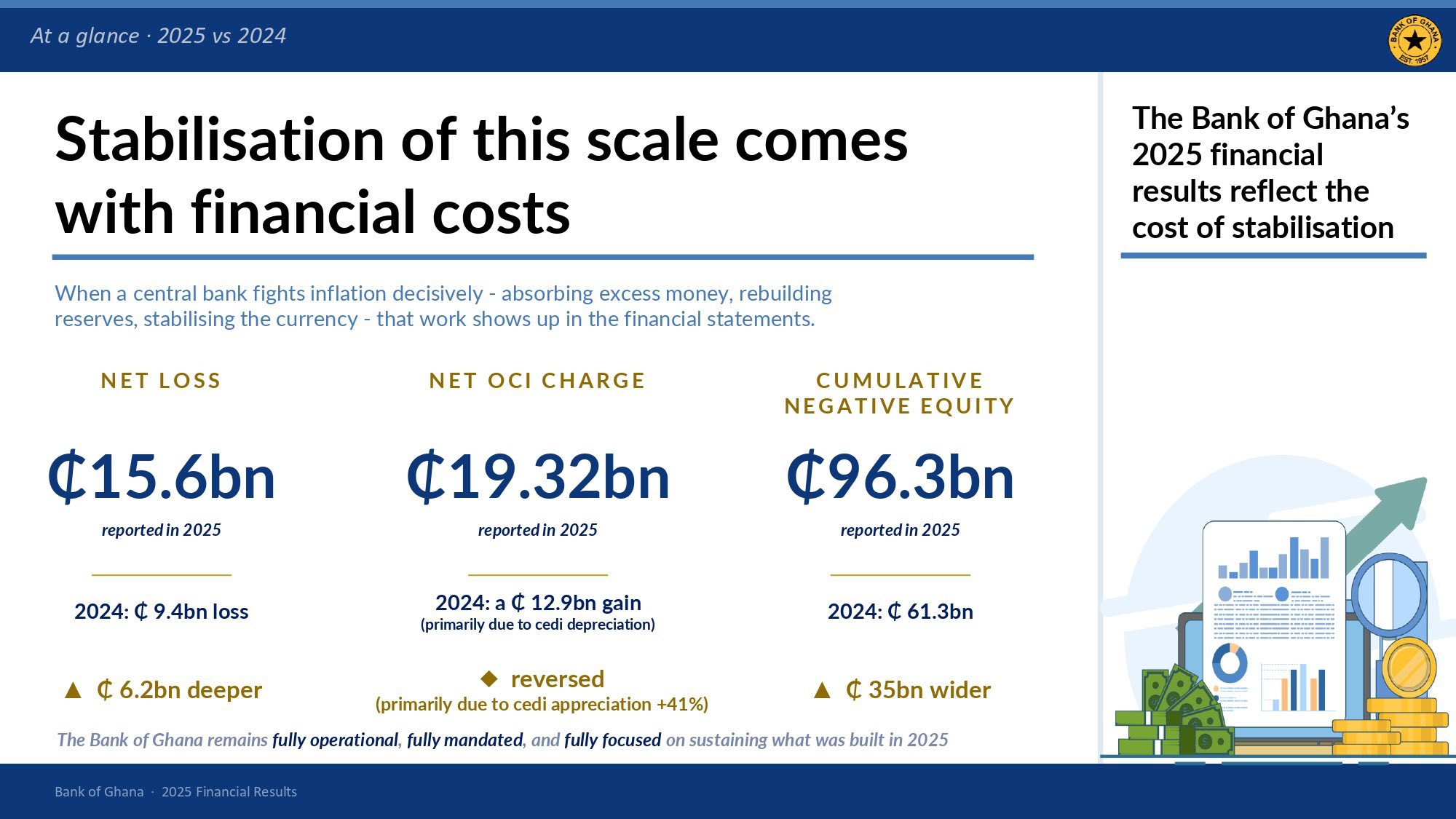

BoG has posted a GH¢15.63 billion operating loss for the 2025 financial year but a careful study of the report shows that without a GH¢9.57 billion gain from refined gold sales, the loss would have exceeded GH¢25 billion.

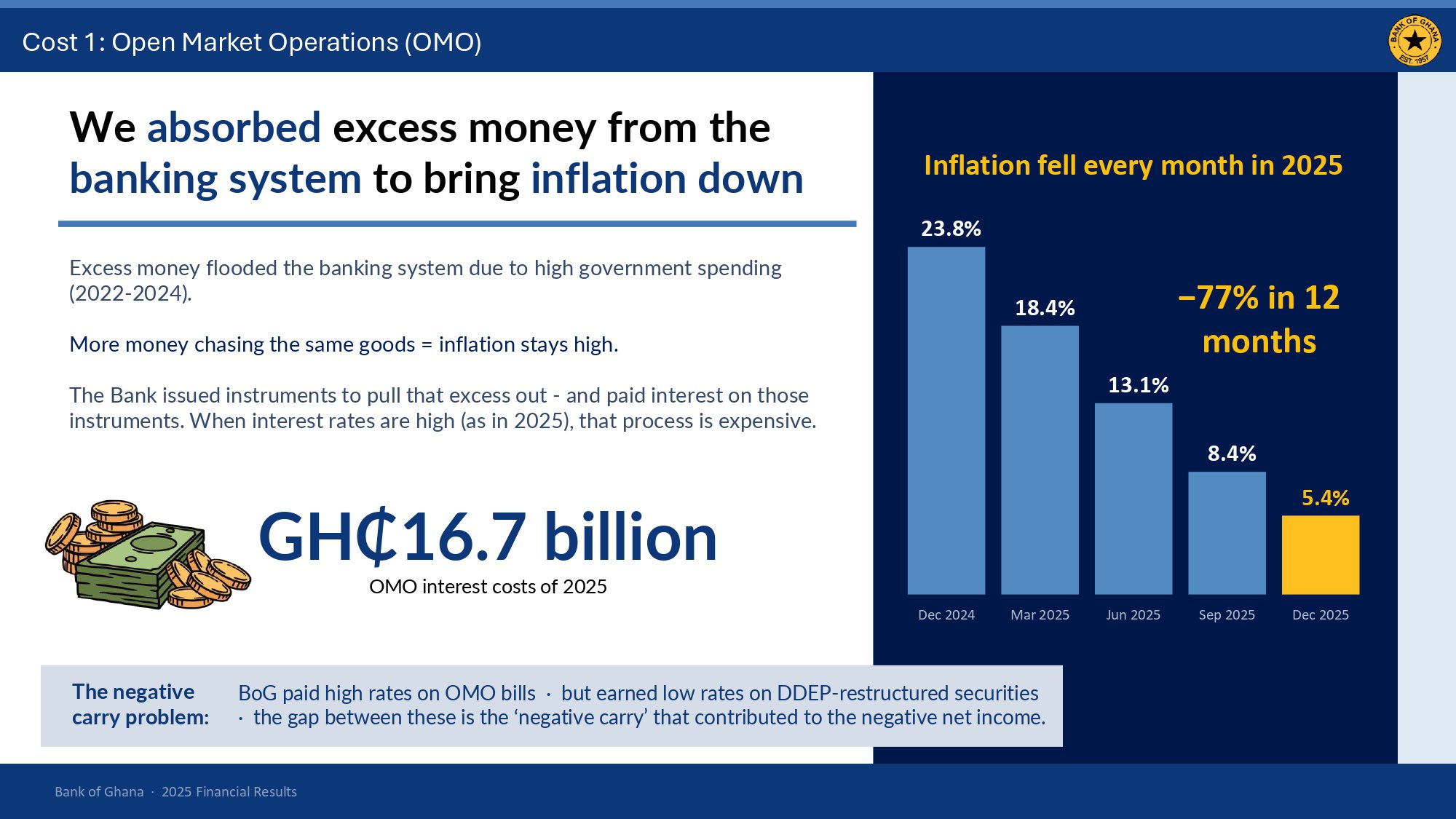

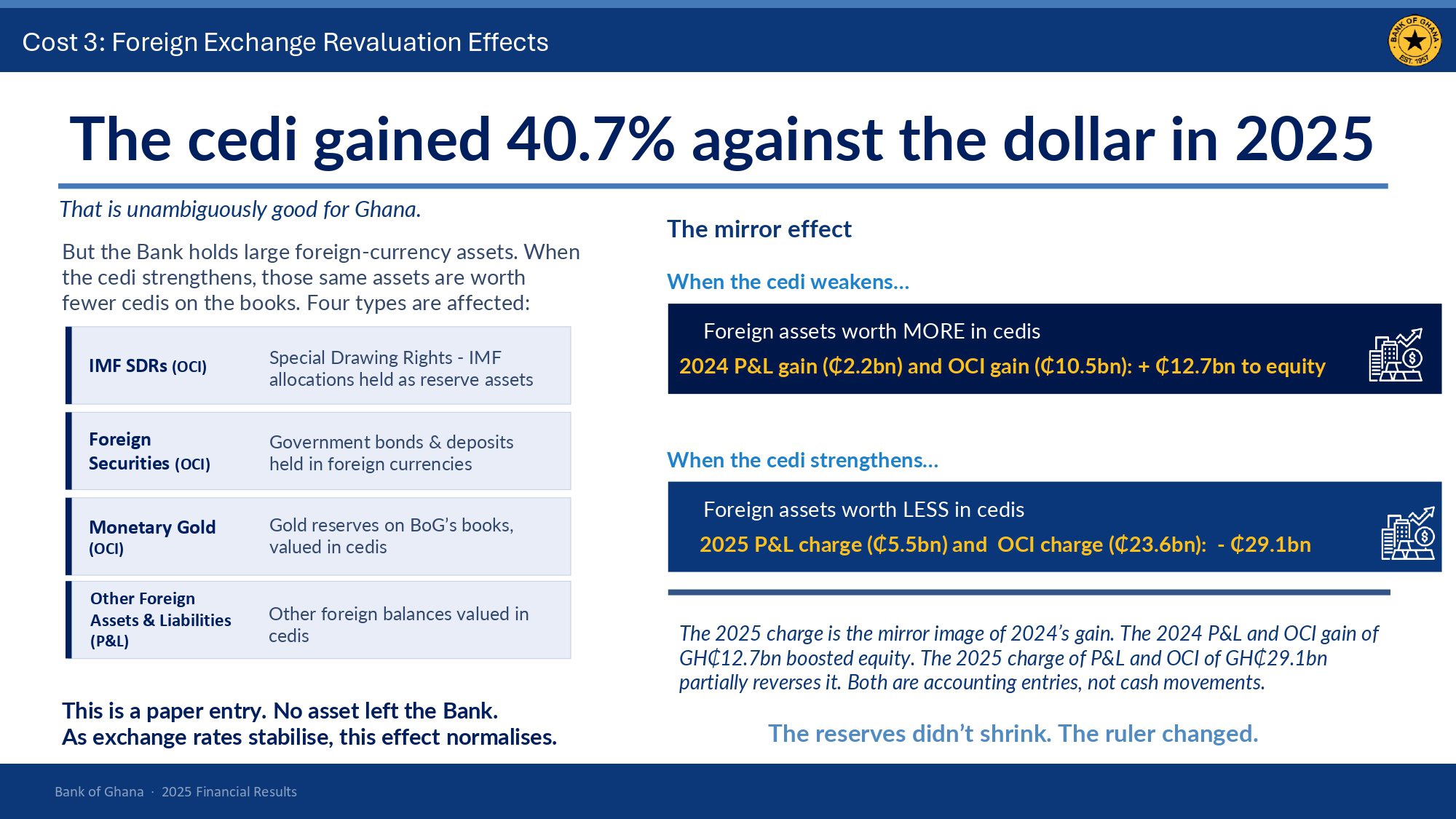

This gap highlights the true cost of anchoring the Cedi and reining in inflation with high interest rates.

This gap highlights the true cost of anchoring the Cedi and reining in inflation with high interest rates.

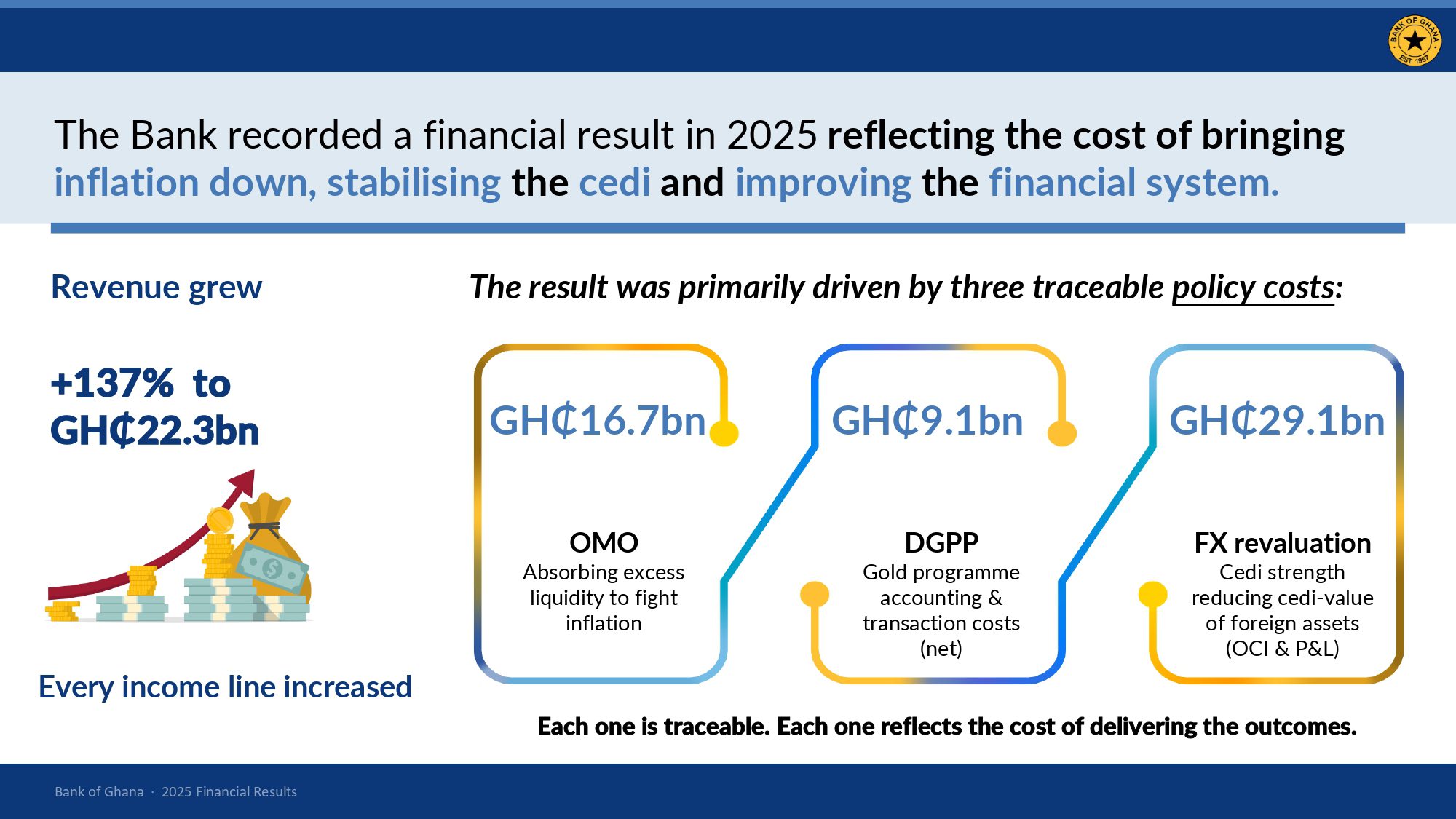

Despite the accounting loss, the Bank however recorded a markedly improved policy solvency position in 2025 compared to 2024.

This was driven by stronger reserve management income, increased fees and commissions from higher transaction volumes and most importantly earnings from gold as part of a broader reserve diversification strategy.

This was driven by stronger reserve management income, increased fees and commissions from higher transaction volumes and most importantly earnings from gold as part of a broader reserve diversification strategy.

Basically, without the gold sale, ability of the Central Bank to fund critical monetary tools such as liquidity absorption would have come under significant strain.

“The Domestic Gold Purchase Programme has contributed meaningfully to the stabilisation of Ghana’s foreign exchange market by strengthening reserve buffers and reducing structural pressures on foreign currency demand. Through the domestic acquisition of gold, the Programme has enabled the Bank to augment foreign exchange reserves without recourse to the domestic foreign exchange market, thereby easing pressure on the cedi”, the report from the Directors of the Bank of Ghana to the Finance Minister mentioned.

“The Domestic Gold Purchase Programme has contributed meaningfully to the stabilisation of Ghana’s foreign exchange market by strengthening reserve buffers and reducing structural pressures on foreign currency demand. Through the domestic acquisition of gold, the Programme has enabled the Bank to augment foreign exchange reserves without recourse to the domestic foreign exchange market, thereby easing pressure on the cedi”, the report from the Directors of the Bank of Ghana to the Finance Minister mentioned.

Since the global financial crisis, central banks have increasingly turned to gold to strengthen reserves and reduce exposure to external shocks.

Since the global financial crisis, central banks have increasingly turned to gold to strengthen reserves and reduce exposure to external shocks.

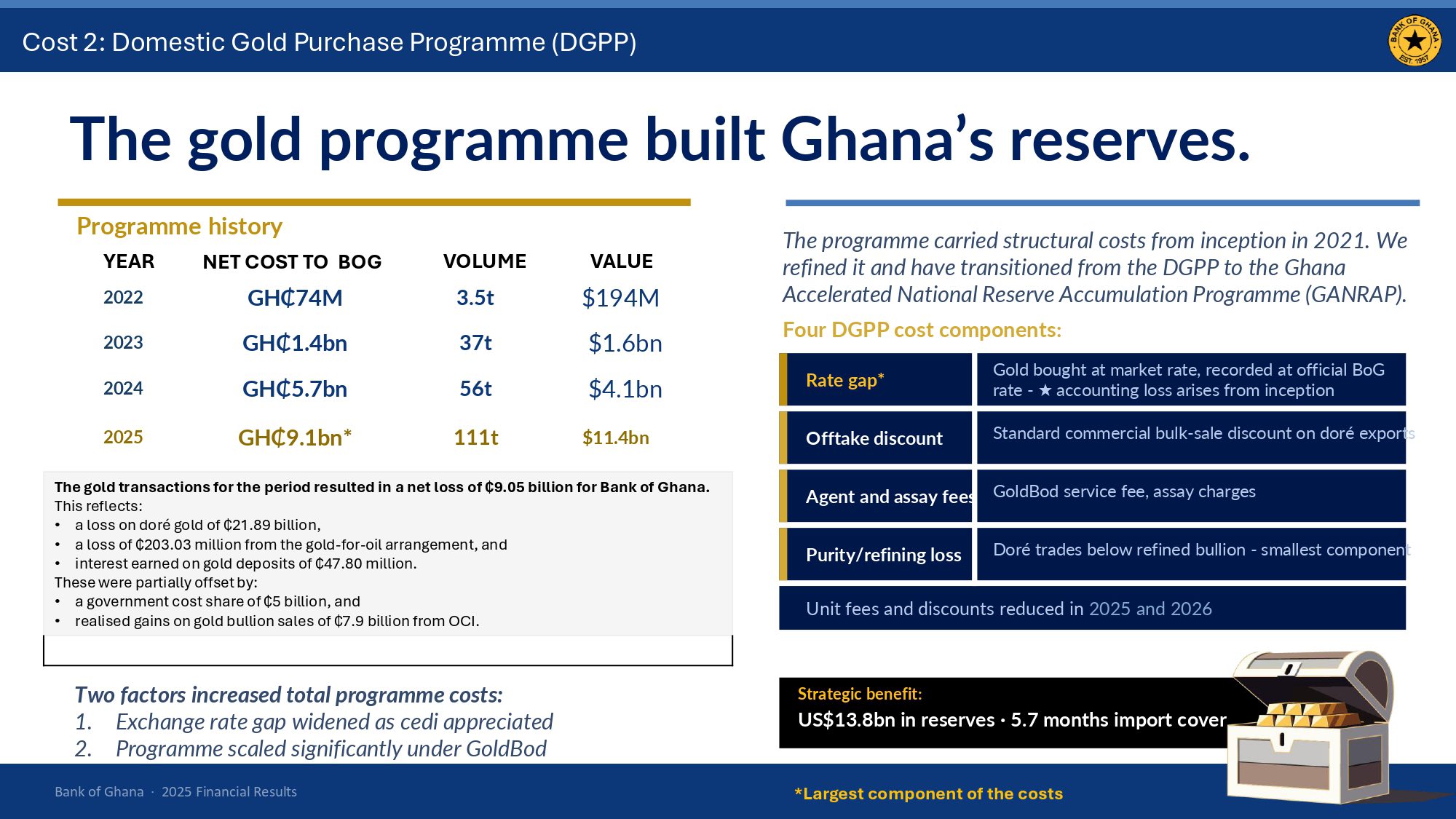

For Ghana, this strategy has been formalized through the Domestic Gold Purchase Programme, launched in June 2021 at a time of mounting economic pressures.

The programme was adopted to rebuild depleted reserves, ease exchange rate pressures and restore investor confidence in the economy.

The programme was adopted to rebuild depleted reserves, ease exchange rate pressures and restore investor confidence in the economy.

Under the initiative, the Bank sources gold through multiple channels including the purchasing of refined gold from mining companies for direct inclusion in reserves.

It acquires dore gold from aggregators for refining into monetary gold and it buys gold from small-scale miners through the Ghana Gold Board for export to generate foreign exchange liquidity.

This layered approach allows the Bank to both accumulate reserves and generate income while maintaining flexibility in managing market interventions.

This layered approach allows the Bank to both accumulate reserves and generate income while maintaining flexibility in managing market interventions.

Since implementation, the Bank has been able to build foreign exchange buffers without drawing heavily on the currency market – a development helping to ease pressure on the local currency.

In addition, the conversion of gold into reserve assets has strengthened reserve adequacy and improved the ability to intermediate during periods of stress.

“Furthermore, the Programme has materially advanced reserve diversification, reduced dependence on other foreign currency denominated assets, and bolstered confidence in the Bank’s external position and overall policy framework. Taken together, these outcomes have contributed to moderating exchange rate volatility and reinforcing stability in the foreign exchange market”, the Directors concluded.

“Furthermore, the Programme has materially advanced reserve diversification, reduced dependence on other foreign currency denominated assets, and bolstered confidence in the Bank’s external position and overall policy framework. Taken together, these outcomes have contributed to moderating exchange rate volatility and reinforcing stability in the foreign exchange market”, the Directors concluded.